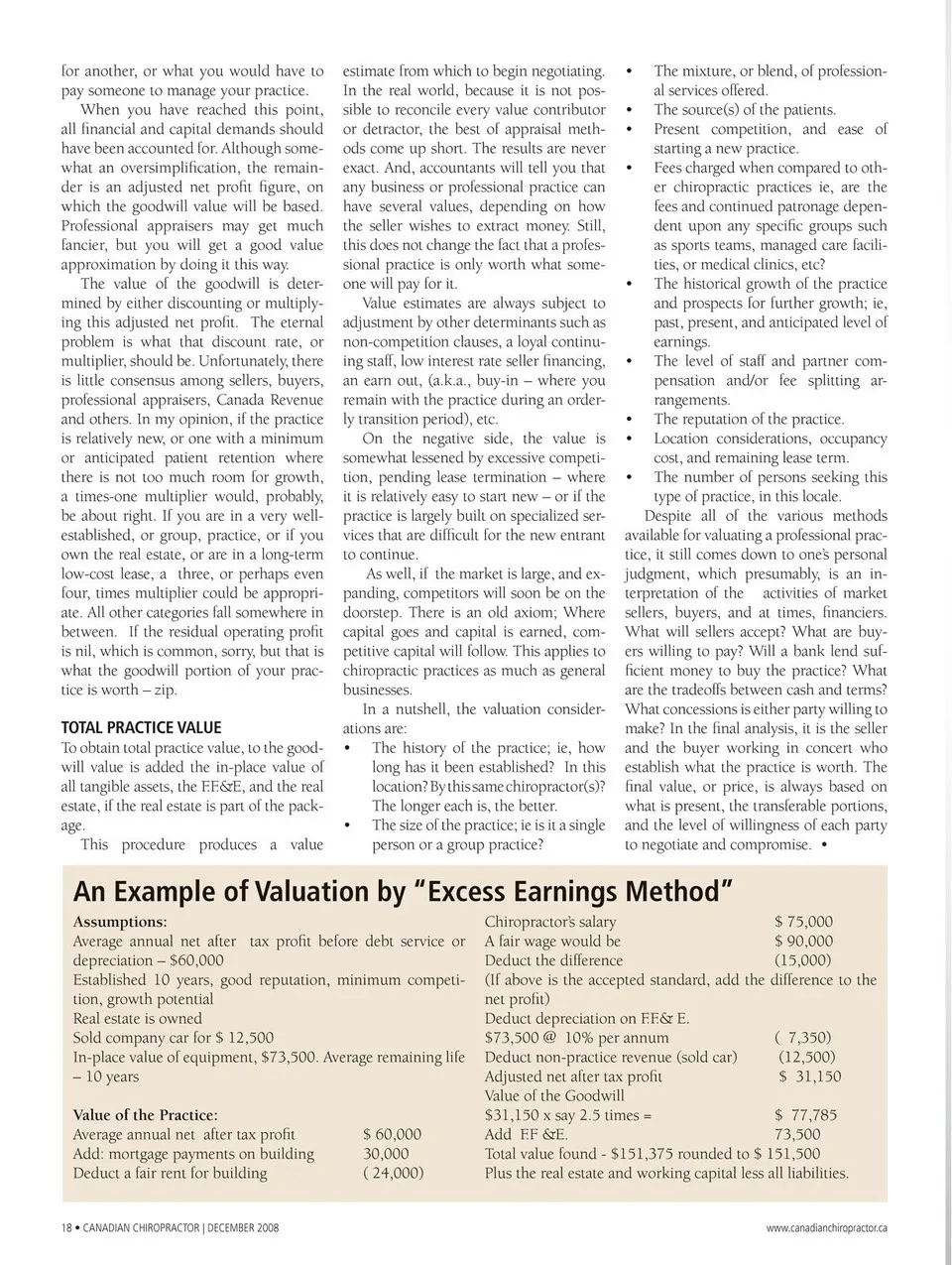

for another, or what you would have to pay someone to manage your practice. When you have reached this point, all fi nancial and capital demands should have been accounted for. Although some- what an oversimplifi cation, the remain- der is an adjusted net profit figure, on which the goodwill value will be based. Professional appraisers may get much fancier, but you will get a good value approximation by doing it this way. The value of the goodwill is deter- mined by either discounting or multiply- ing this adjusted net profi t. The eternal problem is what that discount rate, or multiplier, should be. Unfortunately, there is little consensus among sellers, buyers, professional appraisers, Canada Revenue and others. In my opinion, if the practice is relatively new, or one with a minimum or anticipated patient retention where there is not too much room for growth, a times-one multiplier would, probably, be about right. If you are in a very well- established, or group, practice, or if you own the real estate, or are in a long-term low-cost lease, a three, or perhaps even four, times multiplier could be appropri- ate. All other categories fall somewhere in between. If the residual operating profit is nil, which is common, sorry, but that is what the goodwill portion of your prac- tice is worth – zip. TOTAL PRACTICE VALUE To obtain total practice value, to the good- will value is added the in-place value of all tangible assets, the F.F.&E, and the real estate, if the real estate is part of the pack- age. This procedure produces a value Assumptions: Average annual net after estimate from which to begin negotiating. In the real world, because it is not pos- sible to reconcile every value contributor or detractor, the best of appraisal meth- ods come up short. The results are never exact. And, accountants will tell you that any business or professional practice can have several values, depending on how the seller wishes to extract money. Still, this does not change the fact that a profes- sional practice is only worth what some- one will pay for it. Value estimates are always subject to adjustment by other determinants such as non-competition clauses, a loyal continu- ing staff, low interest rate seller financing, an earn out, (a.k.a., buy-in – where you remain with the practice during an order- ly transition period), etc. On the negative side, the value is somewhat lessened by excessive competi- tion, pending lease termination – where it is relatively easy to start new – or if the practice is largely built on specialized ser- vices that are diffi cult for the new entrant to continue. As well, if the market is large, and ex- panding, competitors will soon be on the doorstep. There is an old axiom; Where capital goes and capital is earned, com- petitive capital will follow. This applies to chiropractic practices as much as general businesses. In a nutshell, the valuation consider- ations are: • The history of the practice; ie, how long has it been established? In this location? By this same chiropractor(s)? The longer each is, the better. • The size of the practice; ie is it a single person or a group practice? • The mixture, or blend, of profession- al services offered. • The source(s) of the patients. • Present competition, and ease of starting a new practice. • Fees charged when compared to oth- er chiropractic practices ie, are the fees and continued patronage depen- dent upon any specifi c groups such as sports teams, managed care facili- ties, or medical clinics, etc? • The historical growth of the practice and prospects for further growth; ie, past, present, and anticipated level of earnings. • The level of staff and partner com- pensation and/or fee splitting ar- rangements. • The reputation of the practice. • Location considerations, occupancy cost, and remaining lease term. • The number of persons seeking this type of practice, in this locale. Despite all of the various methods available for valuating a professional prac- tice, it still comes down to one’s personal judgment, which presumably, is an in- terpretation of the activities of market sellers, buyers, and at times, financiers. What will sellers accept? What are buy- ers willing to pay? Will a bank lend suf- fi cient money to buy the practice? What are the tradeoffs between cash and terms? What concessions is either party willing to make? In the fi nal analysis, it is the seller and the buyer working in concert who establish what the practice is worth. The fi nal value, or price, is always based on what is present, the transferable portions, and the level of willingness of each party to negotiate and compromise. • An Example of Valuation by “Excess Earnings Method” Chiropractor’s salary tax profi t before debt service or depreciation – $60,000 Established 10 years, good reputation, minimum competi- tion, growth potential Real estate is owned Sold company car for $ 12,500 In-place value of equipment, $73,500. Average remaining life – 10 years Value of the Practice: Average annual net after tax profit Add: mortgage payments on building Deduct a fair rent for building 18 • CANADIAN CHIROPRACTOR | DECEMBER 2008 $ 60,000 30,000 ( 24,000) A fair wage would be Deduct the difference $ 75,000 $ 90,000 (15,000) (If above is the accepted standard, add the difference to the net profit) Deduct depreciation on F.F.& E. $73,500 @ 10% per annum Deduct non-practice revenue (sold car) Adjusted net after tax profi t Value of the Goodwill $31,150 x say 2.5 times = Add F.F &E. ( 7,350) (12,500) $ 31,150 $ 77,785 73,500 Total value found - $151,375 rounded to $ 151,500 Plus the real estate and working capital less all liabilities. www.canadianchiropractor.ca

Chiropractic + Naturopathic Doctor December 08: Page 18