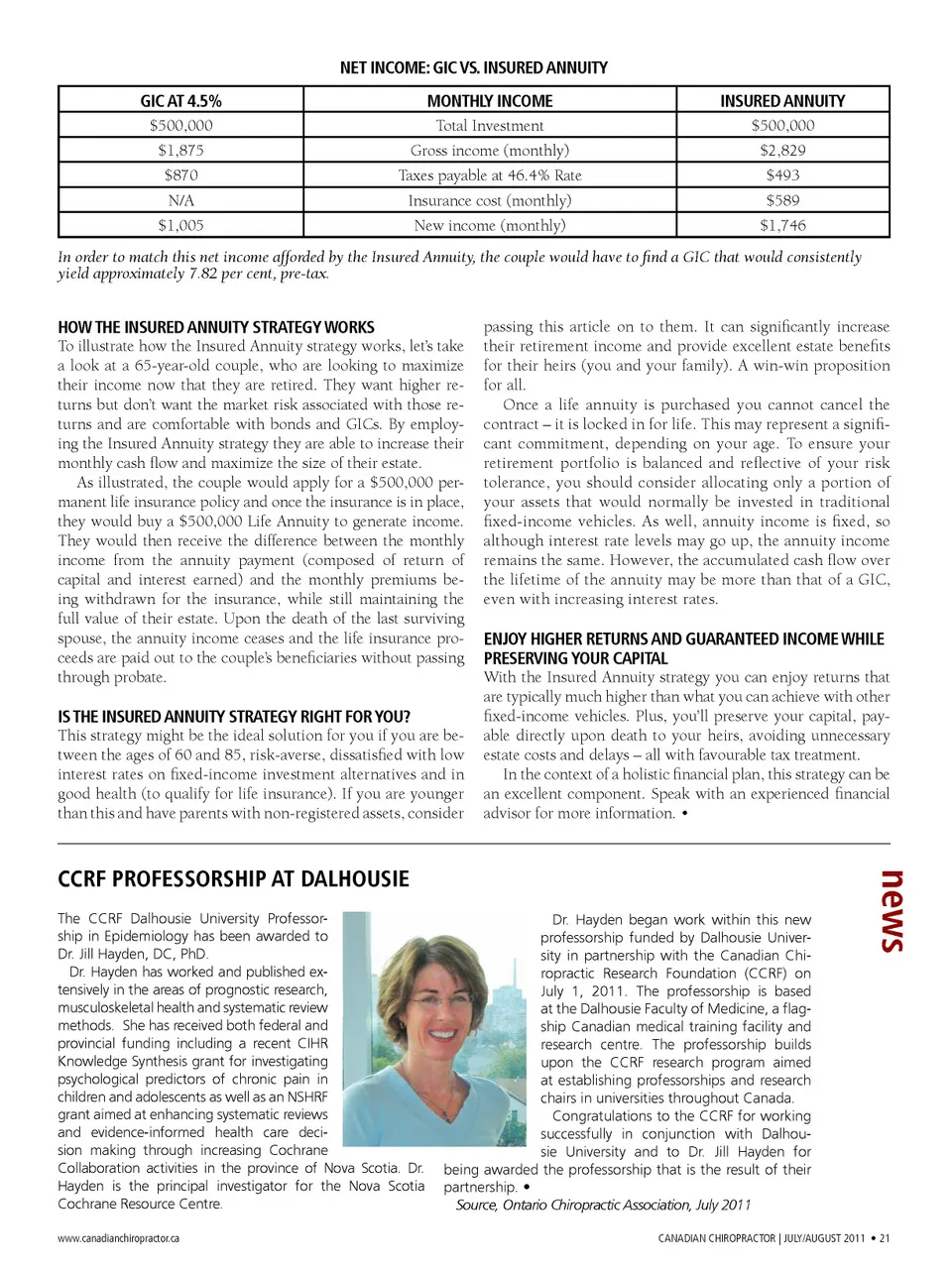

NET INCOME: GIC VS. INSuRED ANNuITY GIC AT 4.5% $500,000 $1,875 $870 N/A $1,005 MONTHLY INCOME Total Investment Gross income (monthly) Taxes payable at 46.4% Rate Insurance cost (monthly) New income (monthly) INSuRED ANNuITY $500,000 $2,829 $493 $589 $1,746 In order to match this net income afforded by the Insured Annuity, the couple would have to find a GIC that would consistently yield approximately 7.82 per cent, pre-tax. HOW THE INSuRED ANNuITY STRATEGY WORKS To illustrate how the Insured Annuity strategy works, let’s take a look at a 65-year-old couple, who are looking to maximize their income now that they are retired. They want higher re-turns but don’t want the market risk associated with those re-turns and are comfortable with bonds and GICs. By employ-ing the Insured Annuity strategy they are able to increase their monthly cash flow and maximize the size of their estate. As illustrated, the couple would apply for a $500,000 per -manent life insurance policy and once the insurance is in place, they would buy a $500,000 Life Annuity to generate income. They would then receive the difference between the monthly income from the annuity payment (composed of return of capital and interest earned) and the monthly premiums be-ing withdrawn for the insurance, while still maintaining the full value of their estate. Upon the death of the last surviving spouse, the annuity income ceases and the life insurance pro-ceeds are paid out to the couple’s beneficiaries without passing through probate. IS THE INSuRED ANNuITY STRATEGY RIGHT FOR YOu? This strategy might be the ideal solution for you if you are be-tween the ages of 60 and 85, risk-averse, dissatisfied with low interest rates on fixed-income investment alternatives and in good health (to qualify for life insurance). If you are younger than this and have parents with non-registered assets, consider passing this article on to them. It can significantly increase their retirement income and provide excellent estate benefits for their heirs (you and your family). A win-win proposition for all. Once a life annuity is purchased you cannot cancel the contract – it is locked in for life. This may represent a signifi-cant commitment, depending on your age. To ensure your retirement portfolio is balanced and reflective of your risk tolerance, you should consider allocating only a portion of your assets that would normally be invested in traditional fixed-income vehicles. As well, annuity income is fixed, so although interest rate levels may go up, the annuity income remains the same. However, the accumulated cash flow over the lifetime of the annuity may be more than that of a GIC, even with increasing interest rates. ENJOY HIGHER RETuRNS AND GuARANTEED INCOME WHILE PRESERVING YOuR CAPITAL With the Insured Annuity strategy you can enjoy returns that are typically much higher than what you can achieve with other fixed-income vehicles. Plus, you’ll preserve your capital, pay-able directly upon death to your heirs, avoiding unnecessary estate costs and delays – all with favourable tax treatment. In the context of a holistic financial plan, this strategy can be an excellent component. Speak with an experienced financial advisor for more information. • CCRF PROFESSORSHIP AT DALHOuSIE The CCRF Dalhousie University Professor-ship in Epidemiology has been awarded to Dr. Jill Hayden, DC, PhD. Dr. Hayden has worked and published ex-tensively in the areas of prognostic research, musculoskeletal health and systematic review methods. She has received both federal and provincial funding including a recent CIHR Knowledge Synthesis grant for investigating psychological predictors of chronic pain in children and adolescents as well as an NSHRF grant aimed at enhancing systematic reviews and evidence-informed health care deci-sion making through increasing Cochrane Collaboration activities in the province of Nova Scotia. Dr. Hayden is the principal investigator for the Nova Scotia Cochrane Resource Centre. www.canadianchiropractor.ca news Dr. Hayden began work within this new professorship funded by Dalhousie Univer-sity in partnership with the Canadian Chi-ropractic Research Foundation (CCRF) on July 1, 2011. The professorship is based at the Dalhousie Faculty of Medicine, a flag-ship Canadian medical training facility and research centre. The professorship builds upon the CCRF research program aimed at establishing professorships and research chairs in universities throughout Canada. Congratulations to the CCRF for working successfully in conjunction with Dalhou-sie University and to Dr. Jill Hayden for being awarded the professorship that is the result of their partnership. • Source, Ontario Chiropractic Association, July 2011 Canadian ChiropraCtor | JULY/AUGUST 2011 • 21

Chiropractic + Naturopathic Doctor July/August 2011: Page 21