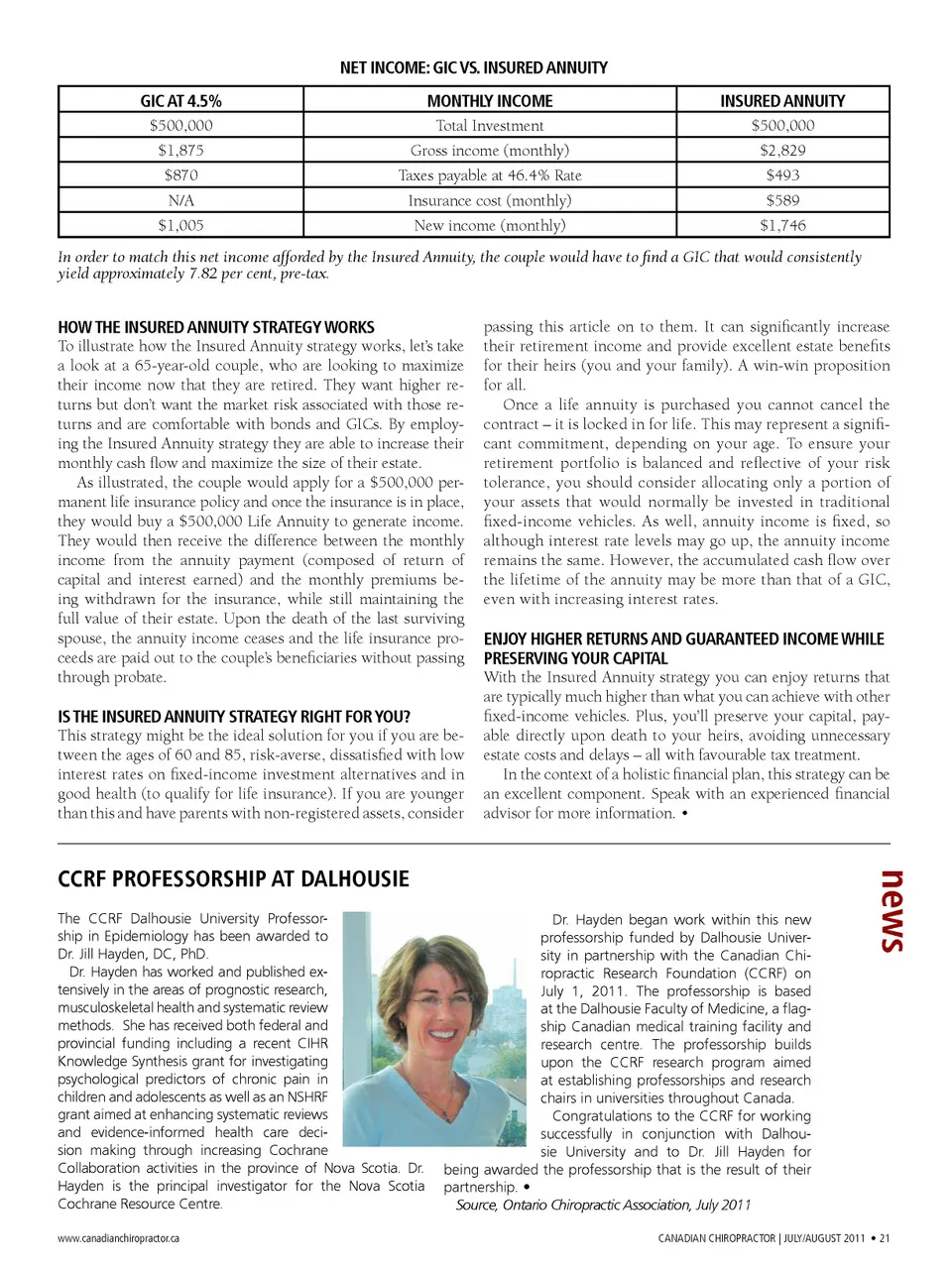

feature Financial Adjustments Insured annuity strategy for increased income with preserved capital W hen it comes to retirement planning, one of the biggest questions most of us face is, “Will I have enough money and will it last?” Traditional investment vehicles such as bonds, T-bills, and GICs are often popular choices to achieve the goals of income gen-eration, safety and preservation of capital in retirement. However, the after-tax rate of return of these options may not provide enough income to meet your needs. Let us share a creative strategy that can result in more income for you in retirement, on a guaranteed basis. Paul Philip CFP, CLU A HIGHER-YIELDING INVESTMENT OPTION WITHOuT MARKET RISK The Insured Annuity strategy provides income that is guaranteed for life, and upon death pays a benefit to your loved ones directly. This strategy can preserve the value of your estate, minimize taxes, and most importantly, guarantee an income stream for the rest of your life, with equivalent returns often much higher than other fixed-income options. ENHANCE YOuR RETIREMENT INCOME AND LEAVE A LEGACY The Insured Annuity strategy involves the purchase of two types of insurance contracts. With the first contract, you purchase a Life Annuity, investing your capital with the in-surance company, and in exchange the insurance company pays you a series of regular, tax-efficient, guaranteed payments for the rest of your life – if you are married, poten-tially, your spouse’s as well. The second contract you purchase is a life insurance policy. A feature of this strategy is that the premiums for the life insurance are paid by a portion of the income generated for the annuity, with no additional costs to you. At death, the annuity income ceases and the life insurance death benefit is paid to your beneficiaries directly (replacing to the estate the value of the capital originally invested in the Life Annuity), without the usual estate-related hassle or costs. The benefits of the Insured Annuity strategy are • It provides guaranteed income for you for the rest of your life (or for you and your spouse’s life) – no matter how long you live; • It significantly enhances the value of your estate and preserves your capital – your beneficiaries receive the insurance proceeds without going through probate; • It protects you against fluctuations in the market – you’ll always know what your income will be no matter how the markets perform; • It is tax efficient – it enhances both your base level of income during retire-ment (only a portion of each annuity payment is taxable, as the remainder is a return of your original investment) and the amount your beneficiaries ultimately receive; • For clients over 65, the interest portion of the annuity income will generally qualify for the Pension Income Amount Tax Credit; • It can help reduce clawbacks of Old Age Security benefits. www.canadianchiropractor.ca Paul Philip, CFP, CLU, and Nancy Philip, CFP, CLU, are a dynamic sib-ling team who have been advising hundreds of chiropractors across Canada since 1992. Their firm, Fi-nancial Wealth Builders, is located in Toronto, Ontario. To learn more about building your wealth, visit their website at www.fwb-inc.com or contact Paul or Nancy at 416-497-0008. Nancy Philip CFP, CLU 20 • Canadian ChiropraCtor | JULY/aUGUSt 2011

Chiropractic + Naturopathic Doctor July/August 2011: Page 20