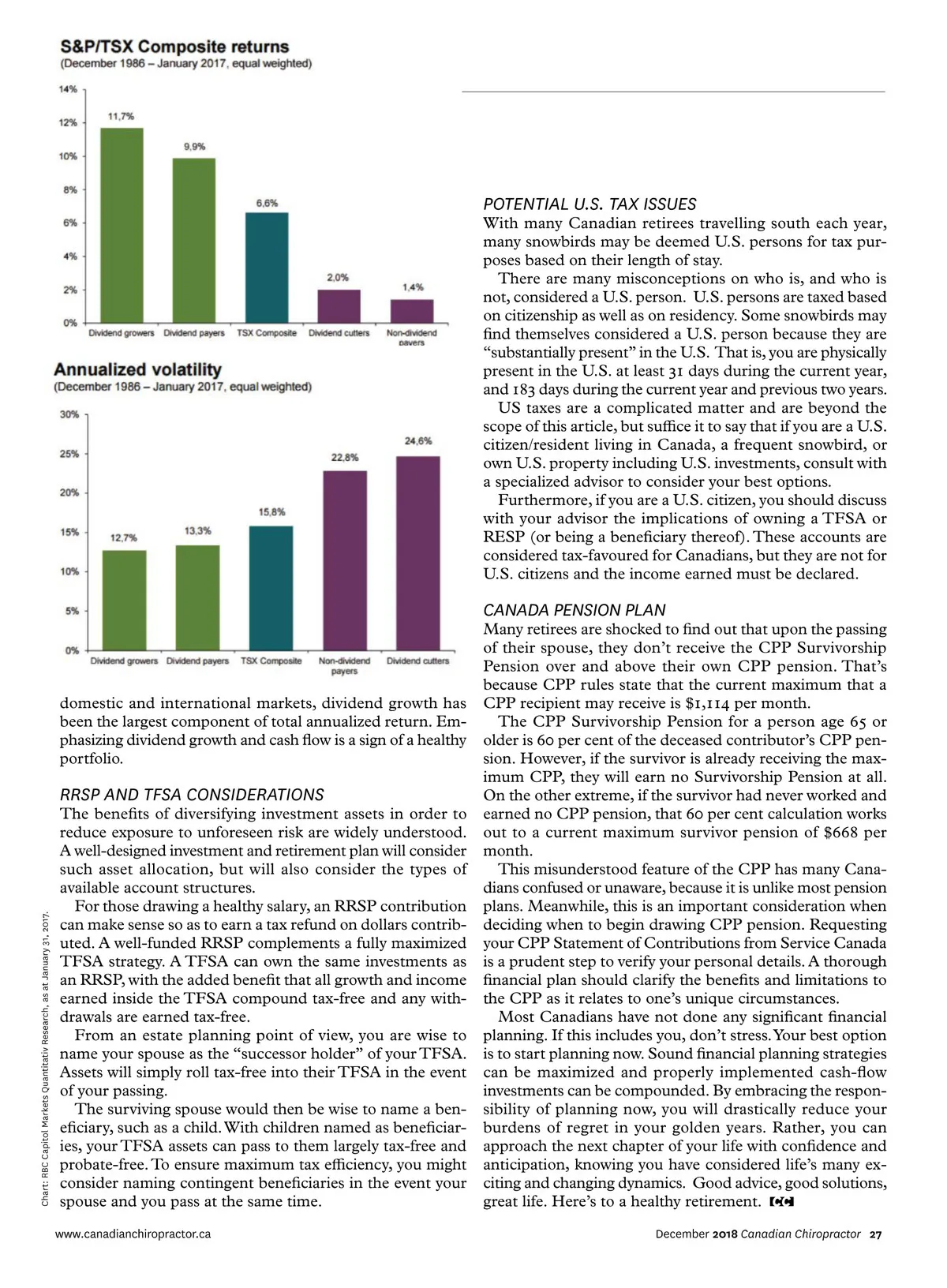

POTENTIAL U.S. TAX ISSUES With many Canadian retirees travelling south each year, many snowbirds may be deemed U.S. persons for tax pur-poses based on their length of stay. There are many misconceptions on who is, and who is not, considered a U.S. person. U.S. persons are taxed based on citizenship as well as on residency. Some snowbirds may find themselves considered a U.S. person because they are “substantially present” in the U.S. That is, you are physically present in the U.S. at least 31 days during the current year, and 183 days during the current year and previous two years. US taxes are a complicated matter and are beyond the scope of this article, but suffice it to say that if you are a U.S. citizen/resident living in Canada, a frequent snowbird, or own U.S. property including U.S. investments, consult with a specialized advisor to consider your best options. Furthermore, if you are a U.S. citizen, you should discuss with your advisor the implications of owning a TFSA or RESP (or being a beneficiary thereof). These accounts are considered tax-favoured for Canadians, but they are not for U.S. citizens and the income earned must be declared. CANADA PENSION PLAN domestic and international markets, dividend growth has been the largest component of total annualized return. Em-phasizing dividend growth and cash flow is a sign of a healthy portfolio. RRSP AND TFSA CONSIDERATIONS The benefits of diversifying investment assets in order to reduce exposure to unforeseen risk are widely understood. A well-designed investment and retirement plan will consider such asset allocation, but will also consider the types of available account structures. For those drawing a healthy salary, an RRSP contribution can make sense so as to earn a tax refund on dollars contrib-uted. A well-funded RRSP complements a fully maximized TFSA strategy. A TFSA can own the same investments as an RRSP, with the added benefit that all growth and income earned inside the TFSA compound tax-free and any with-drawals are earned tax-free. From an estate planning point of view, you are wise to name your spouse as the “successor holder” of your TFSA. Assets will simply roll tax-free into their TFSA in the event of your passing. The surviving spouse would then be wise to name a ben-eficiary, such as a child. With children named as beneficiar-ies, your TFSA assets can pass to them largely tax-free and probate-free. To ensure maximum tax efficiency, you might consider naming contingent beneficiaries in the event your spouse and you pass at the same time. www.canadianchiropractor.ca Many retirees are shocked to find out that upon the passing of their spouse, they don’t receive the CPP Survivorship Pension over and above their own CPP pension. That’s because CPP rules state that the current maximum that a CPP recipient may receive is $1,114 per month. The CPP Survivorship Pension for a person age 65 or older is 60 per cent of the deceased contributor’s CPP pen-sion. However, if the survivor is already receiving the max-imum CPP, they will earn no Survivorship Pension at all. On the other extreme, if the survivor had never worked and earned no CPP pension, that 60 per cent calculation works out to a current maximum survivor pension of $668 per month. This misunderstood feature of the CPP has many Cana-dians confused or unaware, because it is unlike most pension plans. Meanwhile, this is an important consideration when deciding when to begin drawing CPP pension. Requesting your CPP Statement of Contributions from Service Canada is a prudent step to verify your personal details. A thorough financial plan should clarify the benefits and limitations to the CPP as it relates to one’s unique circumstances. Most Canadians have not done any significant financial planning. If this includes you, don’t stress. Your best option is to start planning now. Sound financial planning strategies can be maximized and properly implemented cash-flow investments can be compounded. By embracing the respon-sibility of planning now, you will drastically reduce your burdens of regret in your golden years. Rather, you can approach the next chapter of your life with confidence and anticipation, knowing you have considered life’s many ex-citing and changing dynamics. Good advice, good solutions, great life. Here’s to a healthy retirement. December 2018 Canadian Chiropractor 27 Chart: RBC Capitol Markets Quantitativ Research, as at January 31, 2017.

Chiropractic + Naturopathic Doctor December 2018: Page 27