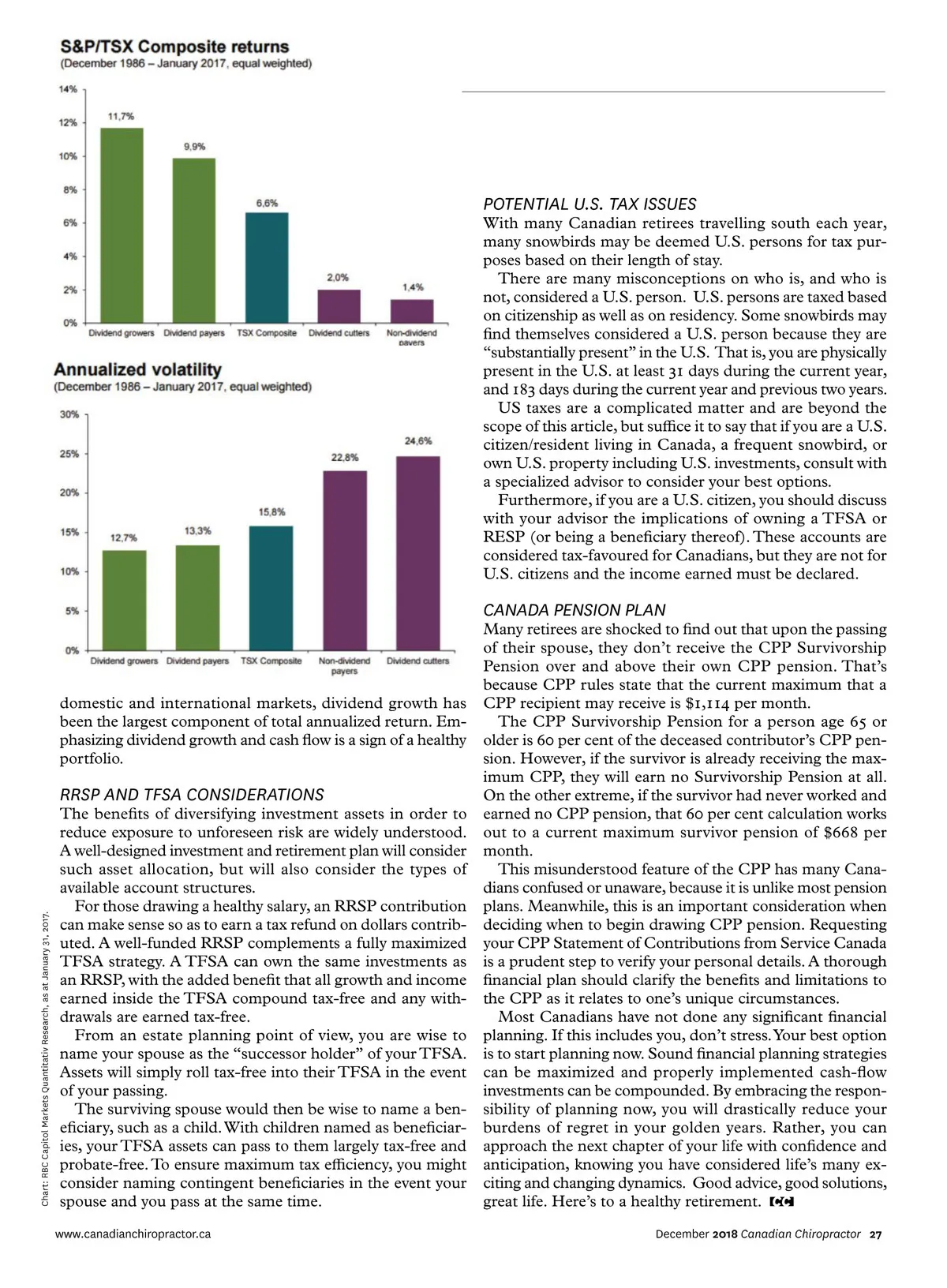

FEATURE FINANCE ARE YOU READY YET? OPPORTUNITIES AND MISCONCEPTIONS OF RETIREMENT PLANNING F BY MIKE MAGREEHAN or most retirees, the thought of retirement al-ways seems to be some destination far off into the future. But like many things in life, retire-ment has a funny way of approaching with greater speed each passing year. Ten million Canadians will retire over the next 20 years. The truth is, some Canadians may outlive their savings, and research shows that this is a greater fear among retirees than dying prematurely. Chiropractors should prioritize the importance of plan-ning for the future, including matching retirement lifestyle expenses with various retirement income streams (variable and guaranteed). In this article we will examine (at a high level) some opportunities and common areas of misconcep-tion in retirement planning. THE BENEFIT OF TIME IS COMPOUNDED WITH CASH FLOW This thought has stuck with me: “You will experience the pain of discipline or the pain of regret. The choice is yours.” The burden of discipline is a fraction of the burden of regret. Of those living with regret, many would pay a hefty price for the luxury of avoiding regret; however, time cannot be rewound. Time is a valuable resource but if left unmanaged, it can be spent and squandered. Where you decide to invest your time shows where you place true value. Whether it be time with family, more MIKE MAGREEHAN is an investment and insurance advisor with Canaccord Genuity Wealth Management in Waterloo, Ont. Mike welcomes your comments and questions at 1.800.495.8071 or mike.magreehan@ canaccord.com. Visit LMwealth.com. 26 Canadian Chiropractor December 2018 leisure, travel, or volunteering for a cause, these are all wor-thy concerns. But in most cases, the constraint of money will determine your effectiveness at fulfilling your goals. According to many academic studies, investing time today into planning your current and future financial affairs will provide fruitful returns on that investment. It has been said that compound interest is the most pow-erful force in the universe. Compound returns only grow in power with time. As such, we encourage a dividend and cash-flow strategy, whereby client investment portfolios are structured so that cash-flow compounds during the working years, with the ultimate intention of paying a handsome cash-flow to one’s bank account in retirement. Consider the following chart, showing the returns on the Canadian market (TSX) from 1986 to current. There are a few things to note: • Dividend-growers returned 11.7 per cent per year (i.e. companies that paid rising dividends over that time period). • Dividend-payers returned 9.9 per cent per year (i.e. companies that paid stable dividends, but didn’t raise or cut their dividends over that time period). Both of these categories provided returns that beat the TSX performance, and did so with less volatility. U.S. research firm Reality Shares, reports similar results for the S&P500. From 1972 to current, dividend-growers returned 9.84 per cent per year and dividend-payers re-turned 7.25 per cent per year with less volatility. In both www.canadianchiropractor.ca

Chiropractic + Naturopathic Doctor December 2018: Page 26