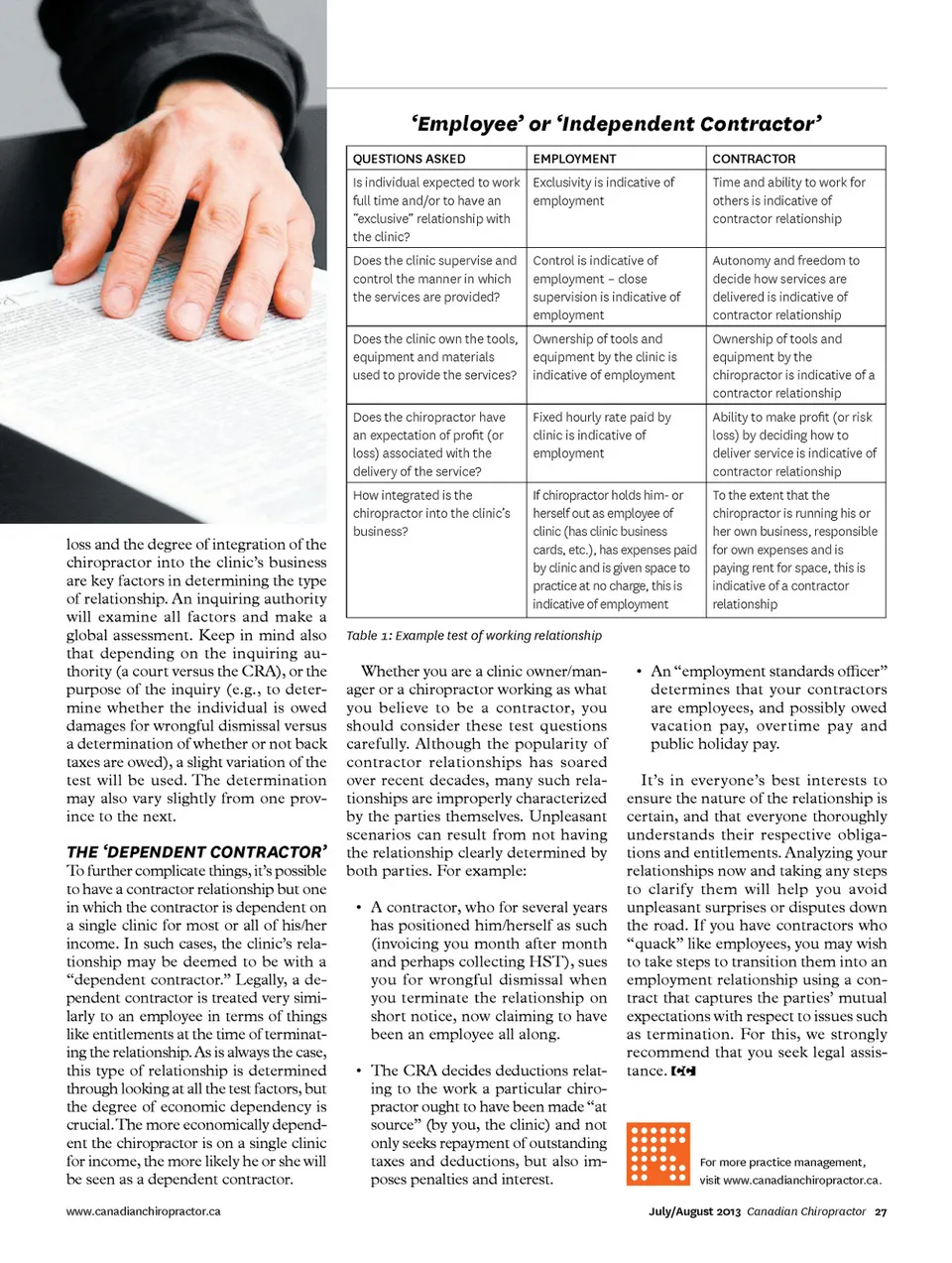

‘Employee’ or ‘Independent Contractor’ Questions Asked employment ContrACtor Time and ability to work for others is indicative of contractor relationship Autonomy and freedom to decide how services are delivered is indicative of contractor relationship Ownership of tools and equipment by the chiropractor is indicative of a contractor relationship Ability to make profit (or risk loss) by deciding how to deliver service is indicative of contractor relationship To the extent that the chiropractor is running his or her own business, responsible for own expenses and is paying rent for space, this is indicative of a contractor relationship Is individual expected to work Exclusivity is indicative of full time and/or to have an employment “exclusive” relationship with the clinic? Does the clinic supervise and control the manner in which the services are provided? Does the clinic own the tools, equipment and materials used to provide the services? Does the chiropractor have an expectation of profit (or loss) associated with the delivery of the service? How integrated is the chiropractor into the clinic’s business? Control is indicative of employment – close supervision is indicative of employment Ownership of tools and equipment by the clinic is indicative of employment Fixed hourly rate paid by clinic is indicative of employment If chiropractor holds him-or herself out as employee of clinic (has clinic business cards, etc.), has expenses paid by clinic and is given space to practice at no charge, this is indicative of employment loss and the degree of integration of the chiropractor into the clinic’s business are key factors in determining the type of relationship. An inquiring authority will examine all factors and make a global assessment. Keep in mind also that depending on the inquiring au-thority (a court versus the CRA), or the purpose of the inquiry (e.g., to deter-mine whether the individual is owed damages for wrongful dismissal versus a determination of whether or not back taxes are owed), a slight variation of the test will be used. The determination may also vary slightly from one prov-ince to the next. To further complicate things, it’s possible to have a contractor relationship but one in which the contractor is dependent on a single clinic for most or all of his/her income. In such cases, the clinic’s rela-tionship may be deemed to be with a “dependent contractor.” Legally, a de-pendent contractor is treated very simi-larly to an employee in terms of things like entitlements at the time of terminat-ing the relationship. As is always the case, this type of relationship is determined through looking at all the test factors, but the degree of economic dependency is crucial. The more economically depend-ent the chiropractor is on a single clinic for income, the more likely he or she will be seen as a dependent contractor. www.canadianchiropractor.ca Table 1: Example test of working relationship THE ‘DEPENDENT CONTRACTOR’ Whether you are a clinic owner/man-ager or a chiropractor working as what you believe to be a contractor, you should consider these test questions carefully. Although the popularity of contractor relationships has soared over recent decades, many such rela-tionships are improperly characterized by the parties themselves. Unpleasant scenarios can result from not having the relationship clearly determined by both parties. For example: • A contractor, who for several years has positioned him/herself as such (invoicing you month after month and perhaps collecting HST), sues you for wrongful dismissal when you terminate the relationship on short notice, now claiming to have been an employee all along. • The CRA decides deductions relat-ing to the work a particular chiro-practor ought to have been made “at source” (by you, the clinic) and not only seeks repayment of outstanding taxes and deductions, but also im-poses penalties and interest. • An “employment standards officer” determines that your contractors are employees, and possibly owed vacation pay, overtime pay and public holiday pay. It’s in everyone’s best interests to ensure the nature of the relationship is certain, and that everyone thoroughly understands their respective obliga-tions and entitlements. Analyzing your relationships now and taking any steps to clarify them will help you avoid unpleasant surprises or disputes down the road. If you have contractors who “quack” like employees, you may wish to take steps to transition them into an employment relationship using a con-tract that captures the parties’ mutual expectations with respect to issues such as termination. For this, we strongly recommend that you seek legal assis-tance. For more practice management, visit www.canadianchiropractor.ca. July/August 2013 Canadian Chiropractor 27

Chiropractic + Naturopathic Doctor July/August 2013: Page 27