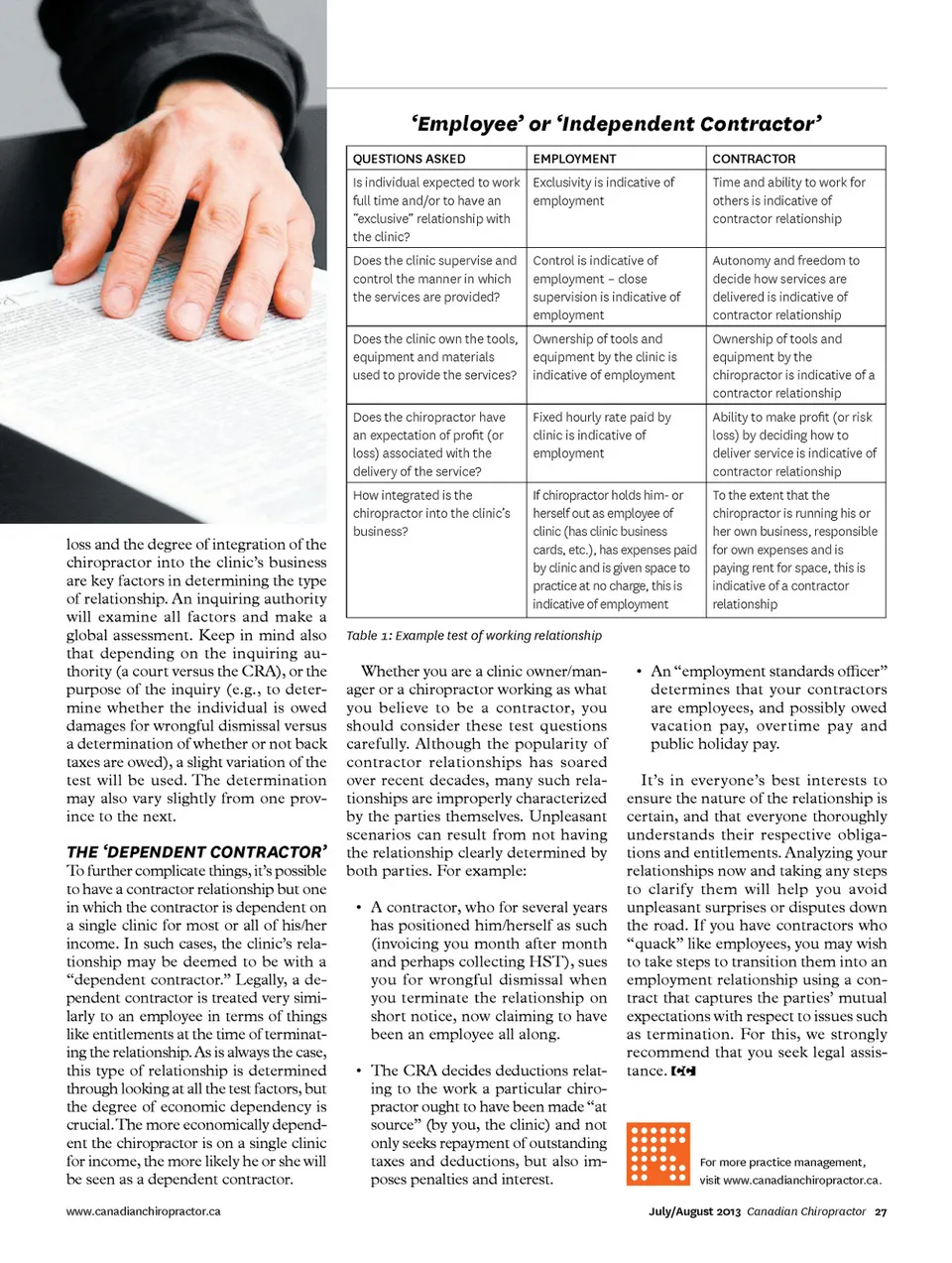

FEATURE PRACTICE MANAGEMENT Chiropractor-clinic relationships They may not be what you think W BY LIOR SAMFIRU AND CHUCK TAHIRALI (up to months’ notice or pay in lieu thereof). Employees have their payroll paperwork and source deductions han-dled for them by the clinic, but contrac-tors handle their own. Contractors can opt out of CPP in some cases, and can deduct business-related expenses at tax time that an employee cannot. Employ-ment relationships and working condi-tions are governed by a complex web of legislation, whereas contractor relation-ships are much less regulated, except by private contract between the parties. relationship. That is, what’s written in a contract is a factor, but it’s rarely determinative. How does one go about determining whether the clinic-chiropractor relation-ship is one of employment or contract? One applies the appropriate variation of the Duck Test – and if the chiropractor walks like an employee and talks like an employee . . . you guessed it. There are several factors involved in this examination. As described in Table , employees are usually paid a fi xed hourly rate or salary, are covered by benefi ts, work a specifi ed number of hours per week, and report to a super-visor who oversees and controls their activities. Typically, employees also have a job title and a clinic business card, use the clinic’s equipment and have busi-ness expenses paid by the clinic. How-ever, if the individual makes decisions about how services are rendered and charged, is paid on a revenue-sharing or other variable basis, is not covered by benefi ts, decides when to work, works for other clinics or o ers independent services to non-clinic clients, works autonomously (free of supervision), covers his/her own business expenses, has his/her own business cards, uses his/ her own equipment and pays rent for the space to practice, the person is more likely to be considered a contractor. Exclusivity, degree of control, owner-ship of tools/equipment, risk of profi t/ www.canadianchiropractor.ca e all know the “Duck Test” – if it looks like a duck, swims like a duck, and quacks like a duck, then it probably is a duck. This test is of great assistance in determining whether the relationship between a clinic and a chiropractor or other professional/ service provider is an employment relationship, or whether the relation-ship is an arm’s length independent contractor relationship. Clinic sta could comprise a mix of employees (from whose wages/salaries the clinic owner makes “source deduc-tions” such as income tax and Employ-ment Insurance premiums) and inde-pendent contractors (responsible for their own deductions and usually col-lect GST-HST). A chiropractor’s re-sumé could include stints as both. There are various advantages and disadvantages to working as either, or having employees or contractors at your clinic. A contractor can be terminated on very short notice (e.g., to days), whereas employees are entitled to much more generous severance entitlements SO, IS IT A DUCK? Are you certain that you’ve entered into the type of relationship you believe you have? What you call yourself or what someone else calls you is com-pletely irrelevant. You may believe your relationship is exactly as specifi ed on the piece of paper you and another party have signed. If so, it may come as a surprise that in the face of a dispute or controversy, the inquiring authority – whether it is the Canada Revenue Agency (CRA), the courts or a govern-ment tribunal such as the Ontario La-bour Relations Board – will defi nitely look beyond what’s stated on that piece of paper to determine the actual legal LIOR SAMFIRU, LLB, heads the Labour and Employment Law practice at Samfiru Tumarkin LLP. Samfiru represents and advises both employees and employers with respect to all workplace matters. CHUCK TAHIRALI, MIR, is a senior human resources consultant and an integral member of the Labour and Employment Group at Samfiru Tumarkin LLP. 26 Canadian Chiropractor July/August 2013 Photo: Dreamstime

Chiropractic + Naturopathic Doctor July/August 2013: Page 26