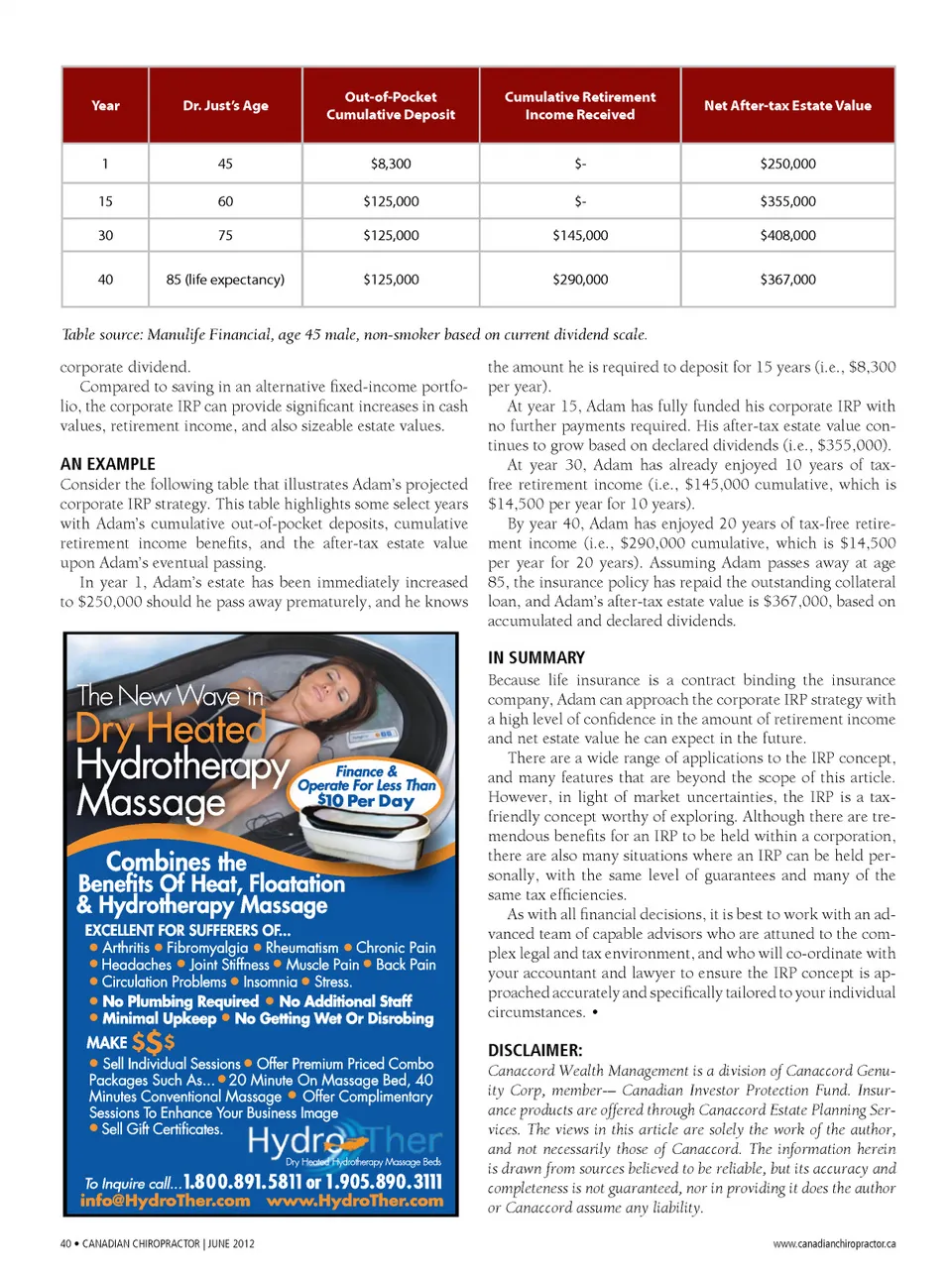

Year Dr. Just’s Age Out-of-Pocket Cumulative Deposit $8,300 $125,000 $125,000 $125,000 Cumulative Retirement Income Received $-$-$145,000 $290,000 Net After-tax Estate Value 1 15 30 40 45 60 75 85 (life expectancy) $250,000 $355,000 $408,000 $367,000 Table source: Manulife Financial, age 45 male, non-smoker based on current dividend scale. corporate dividend. Compared to saving in an alternative fixed-income portfo-lio, the corporate IRP can provide significant increases in cash values, retirement income, and also sizeable estate values. the amount he is required to deposit for 15 years (i.e., $8,300 per year). At year 15, Adam has fully funded his corporate IRP with no further payments required. His after-tax estate value con-tinues to grow based on declared dividends (i.e., $355,000). At year 30, Adam has already enjoyed 10 years of tax-free retirement income (i.e., $145,000 cumulative, which is $14,500 per year for 10 years). By year 40, Adam has enjoyed 20 years of tax-free retire-ment income (i.e., $290,000 cumulative, which is $14,500 per year for 20 years). Assuming Adam passes away at age 85, the insurance policy has repaid the outstanding collateral 4:55 PM loan, and Adam’s after-tax estate value is $367,000, based on accumulated and declared dividends. an eXamPle Consider the following table that illustrates Adam’s projected corporate IRP strategy. This table highlights some select years with Adam’s cumulative out-of-pocket deposits, cumulative retirement income benefits, and the after-tax estate value upon Adam’s eventual passing. In year 1, Adam’s estate has been immediately increased HYDRTHR12-Cdn Chiropractor Ad2 FNL 050712.pdf 1 12-05-11 to $250,000 should he pass away prematurely, and he knows C M Y CM MY CY CMY K in Summary Because life insurance is a contract binding the insurance company, Adam can approach the corporate IRP strategy with a high level of confidence in the amount of retirement income and net estate value he can expect in the future. There are a wide range of applications to the IRP concept, and many features that are beyond the scope of this article. However, in light of market uncertainties, the IRP is a tax-friendly concept worthy of exploring. Although there are tre-mendous benefits for an IRP to be held within a corporation, there are also many situations where an IRP can be held per-sonally, with the same level of guarantees and many of the same tax efficiencies. As with all financial decisions, it is best to work with an ad-vanced team of capable advisors who are attuned to the com-plex legal and tax environment, and who will co-ordinate with your accountant and lawyer to ensure the IRP concept is ap-proached accurately and specifically tailored to your individual circumstances. • diSClaimer: Canaccord Wealth Management is a division of Canaccord Genu-ity Corp, member-– Canadian Investor Protection Fund. Insur-ance products are offered through Canaccord Estate Planning Ser-vices. The views in this article are solely the work of the author, and not necessarily those of Canaccord. The information herein is drawn from sources believed to be reliable, but its accuracy and completeness is not guaranteed, nor in providing it does the author or Canaccord assume any liability. 40 • CANADIAN CHIROPRACTOR | JUNE 2012 www.canadianchiropractor.ca

Chiropractic + Naturopathic Doctor June 2012: Page 40